Delivering Financial Advice With Passion & Integrity

Recession Signals Rising: Inflation, Weak Labor Market & Oil Shock

Recession signals in 2026 are rising as inflation persists, the labor market weakens, and oil prices surge. Read the April 2026 Reber Report.

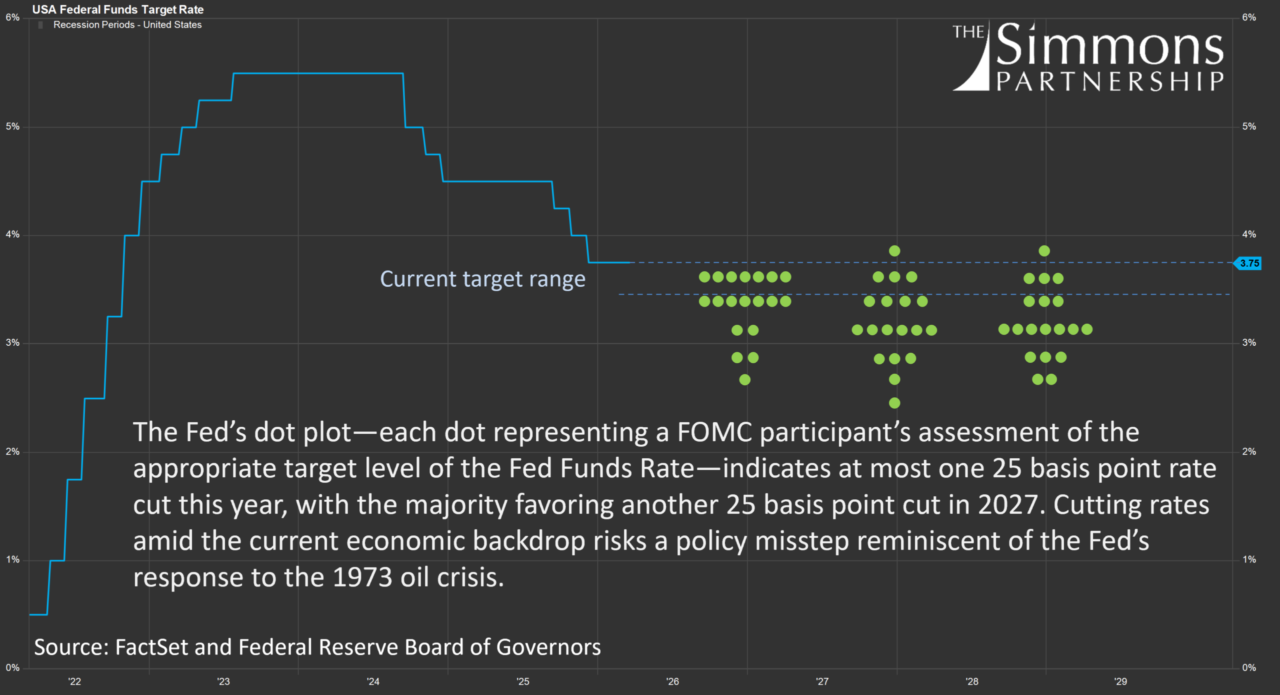

Fed Rate Cuts Would Risk Repeating the Mistakes of the 1970s

The Federal Reserve’s latest decision to hold interest rates steady highlights the increasingly complex economic backdrop. With slowing growth, persistent inflation, and rising geopolitical tensions, policymakers face difficult trade-offs. In this environment, the question isn’t just what the Fed will do next—but whether certain decisions could unintentionally echo past policy mistakes.

The Reber Report Q4 2025 – Reality Check: Asymmetric Risks & Shifting Economic Fundamentals

As we enter 2026, markets and the economy are sending mixed signals. Equity valuations remain elevated and headline GDP growth appears resilient, yet much of that strength has been narrowly driven by AI-related capital investment. Beneath the surface, economic growth has been uneven, inflation remains persistent, and labor market conditions have softened to levels not seen in over a decade.

The U.S. consumer holds the key to the outlook—but confidence trends are at record lows, affordability pressures remain acute, and job growth has weakened. While consumption has ticked up recently, it’s difficult to envision the consumer driving durable growth without meaningful improvement in labor conditions.

Nevertheless, investors shouldn’t underestimate the influence of policy. A more dovish Federal Reserve and fiscal tailwinds could provide support for risk assets in 2026.

In this environment, another year of broad, passive, double-digit equity returns looks unlikely. We believe investors should stay invested, but with greater selectivity—diversifying beyond the AI momentum trade, rotating into overlooked opportunities, and actively managing risk through disciplined portfolio construction, hedging, and liquidity.

Stress in Short-Term Lending Markets is Worth Monitoring

Equity market momentum has decelerated and markets are on pace for their third down week in a row. Interestingly, this pause in equity momentum has coincided with signs of liquidity strains in short-term lending markets. One such signal is the spread between two important short-term interest rates: SOFR and IORB. Large, positive spikes in this spread occurring outside typical quarter-end windows point to potential structural liquidity strains that are worth keeping an eye on.

The Reber Report Q3 2025 – Party Like It’s 1998

U.S. equity markets look eerily like the late 1990s. In Q3 2025, growth is weak, inflation is stubborn, and the Fed is cutting rates despite stretched valuations. The Reber Report warns investors to stay disciplined as risks of a market pullback increase.

Fed Cuts Should Lower Borrowing Costs, Right? Well, Maybe.

Fed rate cuts, labor market weakness, and inflation shape the 2025 economic outlook. Rising Treasury yields may offset policy easing, limiting the impact on mortgages and loans.

Weak GDP Growth Masked as Non-Farm Payrolls Decelerate

Weak GDP Growth Masked as Non-Farm Payrolls Decelerate — that’s the real story behind recent economic data. While headline GDP growth looked solid, deeper numbers show weakening consumption and a slowing labor market. Investors should evaluate their portfolios as markets adjust.

Wills vs. Trusts vs. Beneficiaries: What Every Family Should Know

Understanding how your assets transfer after death is essential to protecting your legacy. This quick guide breaks down the differences between wills, living trusts, and beneficiary designations—helping you avoid probate, minimize delays, and ensure your wishes are honored.

The Reber Report – All That Glitters Is Not Gold

After a rough start to the second quarter, U.S. equity markets staged an impressive rally to get us back to where we were at the beginning of the year. While the recent exuberance may have temporarily quelled investor concerns, the rally is showing signs of stalling out and we see reasons to exercise caution heading into the summer.

Meanwhile, on the economic front, domestic consumption in Q1 was lackluster, the threat of inflationary pressures persists, and cracks are emerging in both the U.S. Treasury market and the labor market. In short, we have effectively returned to the stretched equity valuations we had at the beginning of the year, only with a much less stable economic foundation.

We are not yet in a recession. However, a weakening job market, fiscal and trade uncertainties, persistent inflationary pressures, extremely stretched equity valuations, and increased volatility in financial markets are inconsistent with a thriving economy. Whether or not we end up meeting the technical definition of a recession is largely irrelevant—if current trends continue, we could find ourselves in an environment that feels a lot like one. Investors should govern themselves accordingly.

The Current State of Tariffs

Part of doing the best job we can for you includes complimenting our research with insights from top analyst teams around the world. I believe this overview from one of those teams on the current state of Tariffs is quite insightful, succinct, and balanced. Oftentimes, it’s helpful to restate the information as our industry relies too much on jargon and not enough on straight talk. In this case however, I’m not sure I can represent this topic any better so, here it is in its’ unvarnished state…