Yesterday, the Federal Open Market Committee (FOMC), the Federal Reserve’s policymaking body, announced its decision to hold short-term rates steady, ending the series of three straight rate cuts that closed out 2025.

Both stocks and bonds sold off the past two days, as the move fueled inflation concerns and the Fed’s Summary of Economic Projections signaled fewer than expected rate cuts the rest of this year.

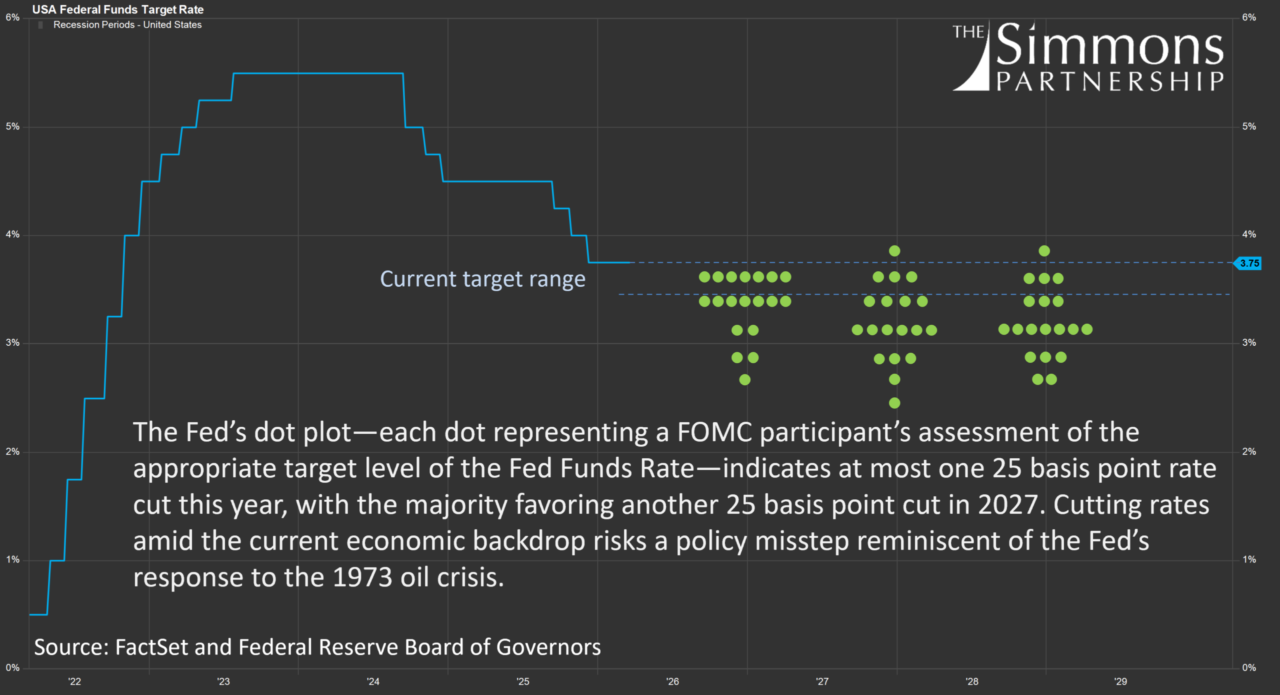

This setup is eerily similar to 1973 when an oil supply shock and Fed missteps fueled inflation and drove the U.S. economy into recession.

How things ultimately play out in the U.S. depends on the duration of the oil shock and the Fed’s policy response.

Read the full post below.

Education is also a core part of what we do. We believe that informed clients are better equipped to stay grounded during periods of market stress and avoid the temptation to make reactive decisions. Through our ongoing commentary, educational series, and client communications, we aim to provide clarity around complex topics without unnecessary noise.

If you found this perspective helpful, we encourage you to explore additional insights available on our blog, including topics such as long-term investing principles, the role of diversification, and how different account types and planning strategies are used in practice.

As always, if you have questions about how current events may—or may not—impact your personal financial situation, we’re here to have that conversation.

Make sure to follow us on our social media platforms. Facebook LinkedIn Instagram