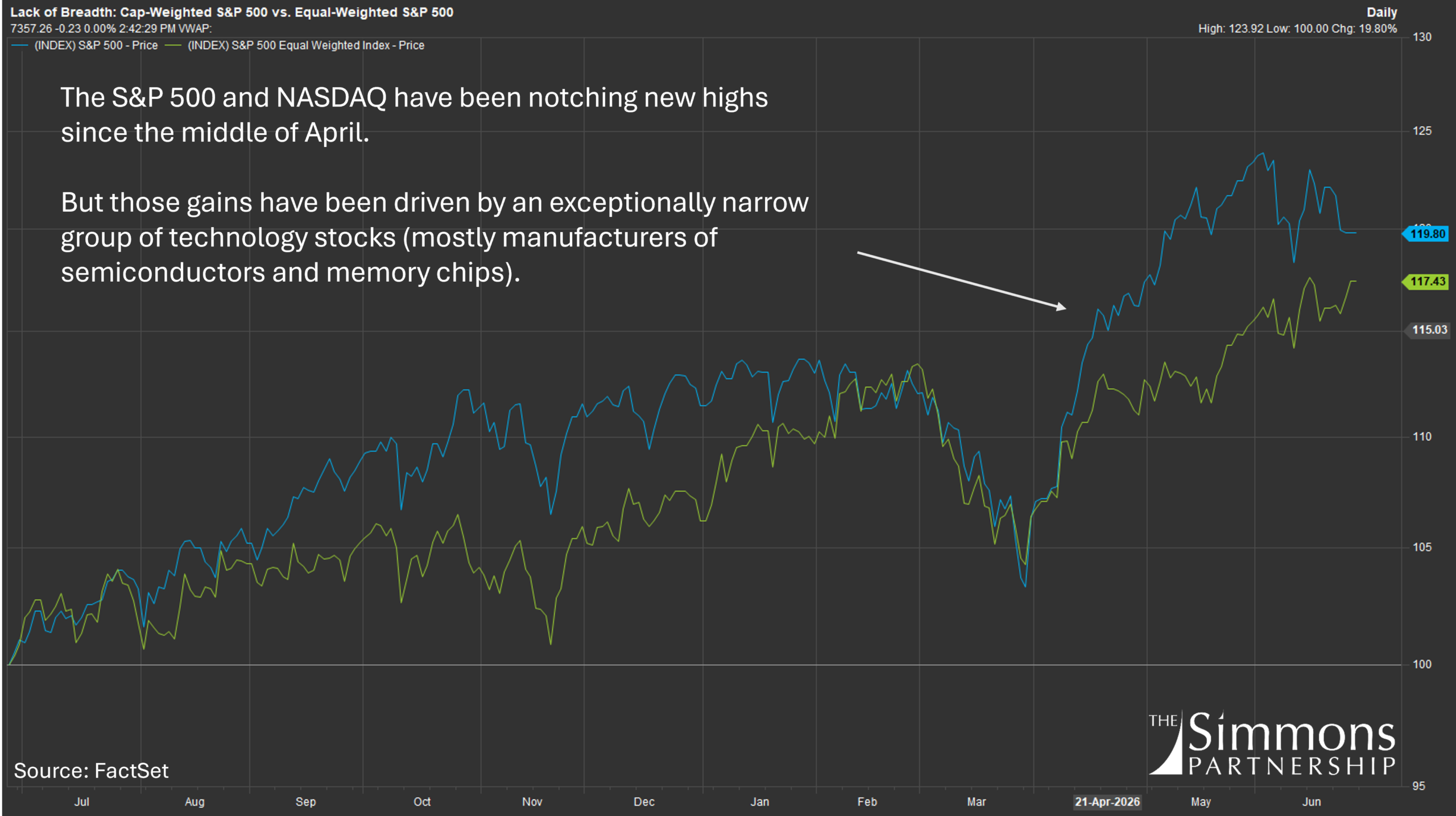

The S&P 500 and NASDAQ have regularly notched new highs since mid-April, yet the vast majority of stocks have not participated in the rally.

At the index level, the advance appears steady, but that is largely a function of how the indexes are constructed. The major indexes are market-cap weighted—that is, larger companies receive a heavier weighting in the index. Those largest companies are also disproportionately in the technology sector, allowing a relatively small number of tech firms to exert an outsized influence on overall index performance. That is precisely what we are seeing in U.S. markets today.

Though we started to see some broadening out of the market rally late last week, leadership has been exceptionally narrow for most of the year, concentrated in a handful of technology companies—particularly manufacturers of semiconductors and memory chips. As a result, the major indexes have become less representative of the performance of the median stock and instead have masked the relatively modest gains and elevated volatility across much of the broader market.

At the end of May, when the S&P 500 was making fresh highs almost daily, Bank of America analysts noted that only about 20 of the 500 stocks in the index—roughly 4%—were also making new highs. That low level of participation highlights just how concentrated the market’s marginal drivers of performance have become. Narrow leadership is not inherently bearish, but it does leave the market increasingly dependent on the continued strength of a very small number of companies.

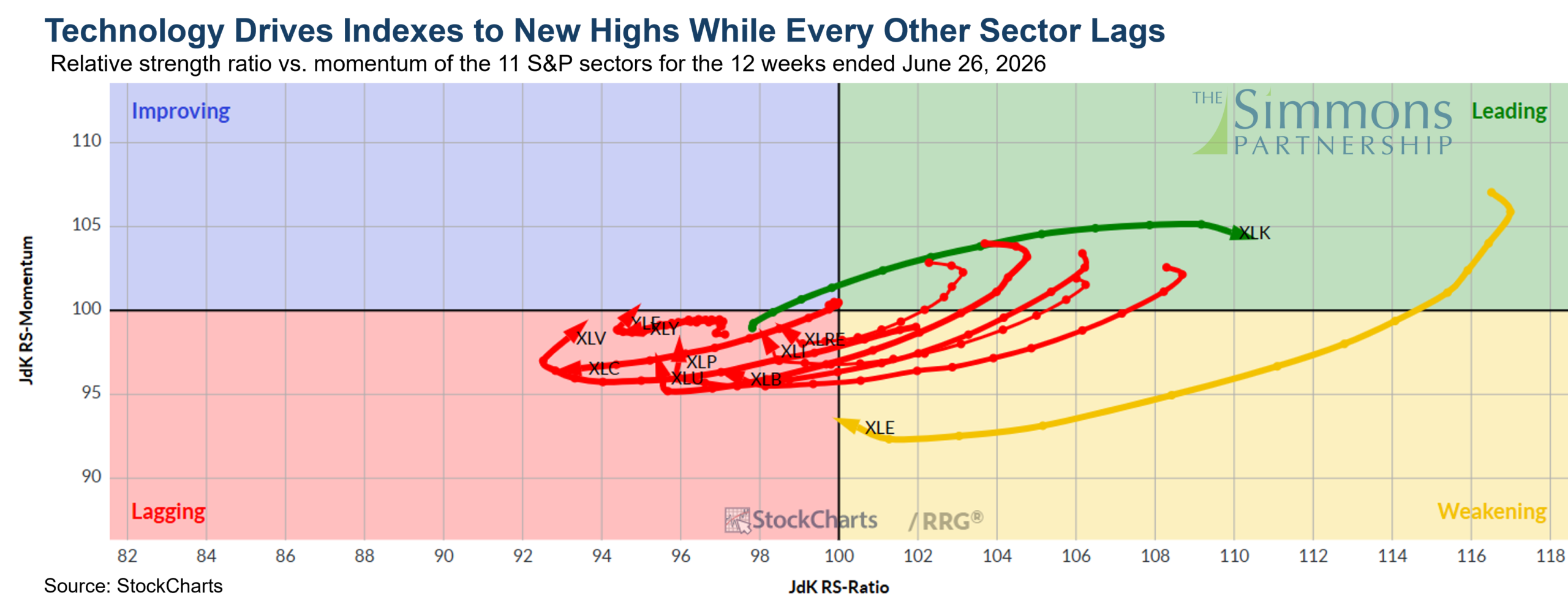

The lack of breadth—the degree to which stocks across the market are participating in a rally—can be seen in both the outperformance of the market-cap weighted S&P 500 relative to the equal-weight S&P 500 (Figure 1) and in the relative strength and momentum of the eleven S&P 500 sectors (Figure 2). This relative rotation graph shows that technology has been the only consistent source of leadership over the past three months, while every other sector has lagged.

That divergence is also evident in market volatility. Index-level volatility has remained relatively subdued because a handful of large constituents dominate index behavior. Individual stocks, however, have experienced much greater variation in returns.

So why not simply own the index? Why do we continue to invest in individual companies?

In a market where leadership is concentrated among only a handful of companies, every new dollar flowing into passive ETFs and index funds allocates additional capital to those same stocks because of their large index weights. Those flows reinforce the outperformance of companies that have already appreciated the most.

In many respects, capitalization-weighted indexing has become a momentum strategy. As companies become larger and their share prices rise, they receive an even greater weighting within the index, attracting additional passive investment. Investors are effectively increasing their exposure to yesterday’s winners based solely on market capitalization rather than underlying fundamentals.

That approach may continue to work. However, based on our fundamental analysis, we believe many of the market’s highest-profile technology companies have become fully valued—or, in some cases, overvalued.

At the same time, we continue to find high-quality businesses with durable competitive advantages, growing revenues, strong earnings, and fortress balance sheets. Healthcare, for example, is a sector where many companies continue to trade at reasonable valuations despite having the potential to benefit significantly from AI-driven improvements in productivity and operating efficiency. While much of the market’s attention has been focused on the companies building AI infrastructure, many of the “old economy” businesses that stand to benefit from AI adoption have been largely overlooked. We believe companies like this this are where the greatest long-term opportunity exists.

Periods of narrow market leadership have historically not lasted indefinitely. While we cannot predict precisely when leadership will broaden, we believe it eventually will. When it does, companies with strong fundamentals and reasonable valuations are likely to benefit. We continue to position portfolios accordingly.

By focusing on fiduciary standards, personalized investment management, and research-driven portfolio construction, The Simmons Partnership aims to help investors make informed long-term financial decisions.

If you found this perspective helpful, we encourage you to explore additional insights available on our blog, including topics such as long-term investing principles, the role of diversification, and how different account types and planning strategies are used in practice.

As always, if you have questions about how current events may—or may not—impact your personal financial situation, we’re here to have that conversation.

Make sure to follow us on our social media platforms. Facebook LinkedIn Instagram

IMPORTANT NOTE FROM THE SIMMONS PARTNERSHIP INC.

This commentary is provided for informational purposes only and does not constitute personalized investment advice or a recommendation to buy or sell any security. Opinions expressed are current as of the publication date and are subject to change. Past performance is not indicative of future results. All investing involves risk, including possible loss of principal. The Simmons Partnership, Inc. is a registered investment adviser. Registration does not imply a certain level of skill or training. Please refer to our Form ADV for additional information regarding our services and fees.